Senior Researcher Park Jae-bum POSCO Research Institute

The Hot Topic of Humanoid Robots! Why Are All-Solid-State Batteries Attracting Attention?

At ‘CES 2026’, held with great enthusiasm earlier this year, the most talked-about topic was humanoid robots. Immediately following the exhibition, interest in humanoid robots surged, leading to a significant rise in the stock prices of robot-related companies. Humanoid robots are designed to perform dangerous or complex tasks in place of humans in workplaces requiring high-intensity labor. Their potential for application across various fields, from daily life to industrial sites, is garnering significant attention.

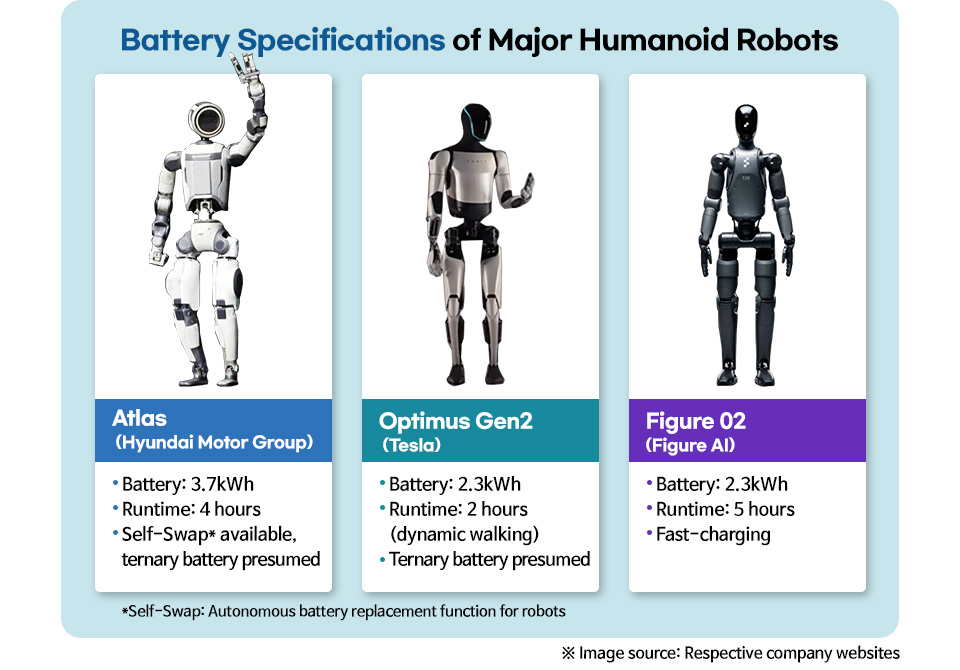

▲ The ‘next-generation electric Atlas research model’ (left) and ‘next-generation electric Atlas open model’ (right) unveiled at CES 2026. Image source: Hyundai Motor Group]

Another hot topic alongside humanoid robots is the all-solid-state battery. An all-solid-state battery is a next-generation battery that replaces the liquid electrolyte, a core material of lithium-ion batteries, with a solid electrolyte. Thanks to the use of a solid electrolyte, it possesses high safety, and based on this, it allows for the improvement of other materials, enabling an increase in the battery’s energy density. In other words, it is one of the suitable battery candidates that meets the energy density and safety requirements demanded by humanoid robots.

Robots, especially humanoids, have limited space for battery installation. Unlike electric vehicles (EVs), it is difficult to mount a large amount of batteries, which limits battery capacity. Therefore, batteries with high energy density per weight and volume are essential for robots. Additionally, since robots must be able to lift heavy objects and perform quick movements instantaneously, high power output is also expected to be a critical factor in battery performance. While all-solid-state batteries are evaluated as capable of meeting these requirements in the future, they are still in the pre-commercialization stage and are currently very expensive.

However, when looking at the proportion of the battery in the total cost, there is a clear difference between EVs and robots. Unlike EVs, where the battery cost accounts for a relatively high portion, the price proportion of the battery in robots is relatively low. Therefore, even if an all-solid-state battery is installed, the price increase for the robot is smaller than that for an EV. For this reason, humanoid robots are being discussed as a promising initial application field once all-solid-state batteries are commercialized.

Between Expectation and Reality… Barriers That All-Solid-State Batteries Must Overcome

Despite these technical advantages and high market expectations, it is difficult for all-solid-state batteries to lead to immediate commercialization in the short term. Even setting aside the problems to be solved in the mass production process, the barrier of high cost still exists.

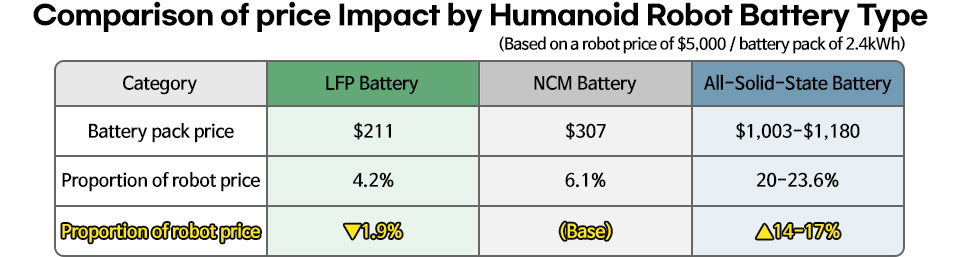

Assuming the commercialization price of a humanoid robot is $5,000 per unit, even if the battery is switched from a ternary NCM (nickel, cobalt, manganese) battery to an LFP battery, the price reduction for the robot is only about 1.9%. In other words, because robots use a small amount of batteries per unit, it is difficult to expect the same cost-saving effect as in EVs by using LFP. What if an all-solid-state battery is applied? It is estimated that the robot price would increase by about 14–17%, and the cost proportion of the battery would rise to the 20–24% level.

Although it varies depending on the characteristics and use of the robot, the industry considers a battery cost share of around 10% to be appropriate for humanoid robots. This is because, in addition to the battery—the heart of the humanoid—there are many other necessary parts and modules, such as actuators (joints), grippers (hands), and AI (the brain), making it difficult to allocate a large portion of the cost to the battery. Therefore, even assuming a maximum cost proportion of 15% considering the performance improvement of the robot due to the application of an all-solid-state battery, the price of all-solid-state batteries needs to drop to the $350/kWh level.

Key challenges for the commercialization of all-solid-state batteries

The main reason for the high price of all-solid-state batteries is the lack of a stable mass production system, but the high price of the core material, solid electrolyte, is also a major factor. The cost of the solid electrolyte material alone exceeds the price of a lithium-ion battery. This is because the price of lithium sulfide (Li₂S), the core raw material for solid electrolytes, remains high at about $500/kg, and because they are mainly manufactured in lab or pilot lines, the ‘economies of scale’ effect—where the average price decreases as production volume increases—has not yet occurred. For all-solid-state batteries to secure price competitiveness compared to lithium-ion batteries, the price of solid electrolytes appears to need to drop to the $30/kg level.

For commercialization, technical challenges remain in addition to price. While improving the safety of all-solid-state batteries is possible just by applying the core solid electrolyte material, improving other materials is also necessary to ultimately increase energy density. Furthermore, to improve peak output (lasting from a few seconds to tens of seconds), technical hurdles such as improving ionic conductivity and overcoming interface resistance must be resolved. Currently, major global companies are actively pursuing material-centered R&D to overcome these limitations.

Despite various issues, all-solid-state batteries are still considered a very suitable next-generation battery technology for robots. This is because they are not only safer than LFP batteries but also have significant room for improvement in energy density. This is expected to improve not only the robot’s operating time but also its peak output performance, which lasts from a few seconds to tens of seconds. Ultimately, whether the substantial improvement in robot performance—such as energy density, peak output, and safety—is clearly proven to offset the burden of increased costs due to the application of all-solid-state batteries will be the key criterion for judging future commercialization.

‘Dream Battery’ All-Solid-State Battery, Can It Accelerate the Timing of Commercialization?

All-solid-state batteries have long been called the ‘dream battery’ and have received high expectations in the secondary battery market, but they still face the challenge of securing mass-producibility and price competitiveness similar to that of lithium-ion batteries. Until now, suitable demand sources for all-solid-state batteries have been limited, but recently, the possibility that the market opening time could be advanced, defying previous expectations, has been raised.

① Before Electric Vehicles? The Potential for Robot Market Application

Among domestic battery manufacturers, Samsung SDI has presented a relatively concrete timeline for the mass production of all-solid-state batteries. The company is targeting 2027 for mass production and is reportedly reviewing the potential for application in various new fields, including robotics. If these plans materialize, all-solid-state batteries could be adopted in non-automotive sectors—such as robotics—before they are widely used in electric vehicles. In particular, because the sample testing and certification processes for robots are relatively more flexible than those for EVs, there is significant potential for the market landscape to shift rapidly.

② China’s Announcement of National Standards for All-Solid-State Batteries

Meanwhile, changes in the global policy environment are acting as a catalyst to accelerate the opening of the all-solid-state battery market. The Chinese government recently announced national standards for all-solid-state batteries, establishing clear terminology and a classification system. This is interpreted as a strategic move to secure market leadership, with a focus on next-generation applications such as robots and eVTOLs*. Major Chinese battery firms are accelerating development with a goal of commercialization around 2027; if coupled with government support, the initial cost burden is expected to be partially mitigated. These national standards and policy supports are significant, as they can accelerate market formation regardless of the current level of technical maturity. In response, Korea is also seeking policy measures, such as securing production bases for core materials and expanding R&D support for next-generation batteries.

*eVTOL (Electric Vertical Take-Off and Landing): An aircraft that uses electric power to hover, take off, and land vertically.

③ The Time Until Commercialization: The Importance of a ‘Pivot Strategy’

The price of all-solid-state batteries during the initial mass production and pilot stage in 2027 is estimated at $400–600/kWh, and a transition to full-scale commercial production is likely to occur only after 2030. However, it is expected that all-solid-state batteries will periodically emerge as a key market topic over the next three to four years, with the construction of material supply chains proceeding in parallel. In this rapidly changing environment, experts argue for the necessity of a ‘pivot strategy*.’ This means that rather than simply waiting for the all-solid-state battery market to open, companies must strengthen their existing lithium-ion battery competitiveness while simultaneously preparing to pivot quickly to all-solid-state technology as the market evolves.

*Pivot: A strategy of changing direction or focus while maintaining the existing core business.

POSCO Group Preparing for the Era of All-Solid-State Batteries

POSCO Group has been preemptively conducting research, development, and investment in core materials such as cathode materials for all-solid-state batteries, lithium-metal anodes, and solid electrolytes. To secure competitiveness in the solid electrolyte business, which is the core of all-solid-state batteries, POSCO Group invested a 40% stake in Jeong-Kwan Co., Ltd. in February 2022 to establish POSCO JK Solid Solution. The company is currently operating a pilot plant and is conducting sample tests for global battery companies and OEMs.

In addition, POSCO Group is accelerating the development of next-generation materials—such as solid electrolytes, high-capacity cathodes, and silicon anodes—through strategic partnerships and equity investments in industry leaders like Taiwan’s ProLogium and the U.S.-based Factorial Energy. Furthermore, the group is moving to internalize the production of lithium sulfide, a core raw material for sulfide-based solid electrolytes, to drive down costs and secure a more economical supply chain.

▲ Panoramic view of POSCO Future M’s Pohang cathode material plant.

Recently, POSCO Future M signed an MOU with Factorial, an all-solid-state battery company headquartered in Massachusetts, USA, for the development of all-solid-state battery technology. Through this cooperation, it is expected that POSCO Future M’s material technology and Factorial’s global partnership capabilities will be combined to secure competitiveness in the all-solid-state battery market.

As such, POSCO Group plans to continuously expand its portfolio of core materials for all-solid-state batteries, including cathode materials for all-solid-state batteries, silicon/lithium-metal anode materials, and sulfide-based solid electrolytes, centered on POSCO Future M, which possesses material design and coating technologies.